After a record-breaking yr in 2024, the U.S. neighborhood photo voltaic market slowed within the first half of 2025, with installations declining 36% year-over-year, leading to 437 MWDC of latest capability put in, in accordance with a brand new report launched by Wood Mackenzie in collaboration with the Coalition for Community Solar Access (CCSA).

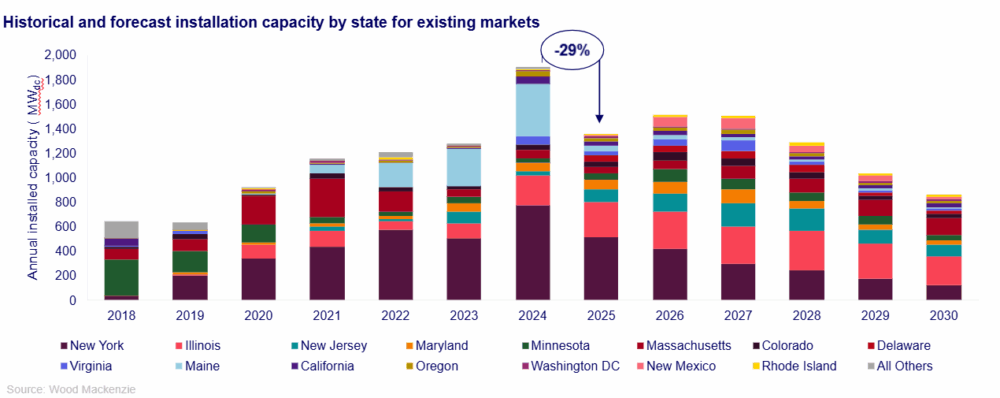

As a result of passage of HR1 and associated federal coverage modifications, Wooden Mackenzie’s cumulative five-year neighborhood photo voltaic outlook decreased by 8% in comparison with the outlook revealed in Q2 2025. HR1 has essentially altered the long-term market panorama, whereas slowing development in mature markets, significantly New York’s neighborhood photo voltaic program, is contributing to an anticipated 29% nationwide contraction in 2025.

“Total, we anticipate nationwide put in neighborhood photo voltaic capability will contract by a mean of 12% yearly by means of 2030,” stated Caitlin Connelly, senior analyst and lead writer of the report. “The ultimate invoice affords an important four-year window for tasks already below growth to return on-line and safe the investment tax credit (ITC), supporting near-term buildout. As of mid-2025, there are over 9 GWDC of neighborhood photo voltaic tasks below growth, with over 1.4 GWDC identified to be below building.”

Credit score: Wooden Mackenzie

Development in rising markets slows and new markets face challenges

In line with the report, the market contraction within the first half of 2025 is primarily pushed by steep declines in volumes in New York and in Maine, the place the present program was just lately overhauled. Packages in some state markets are near or at capability, and a number of other packages in states together with Maryland, Massachusetts and New Jersey stay stalled in transitions between program iterations.

“The early expiration of the ITC will solely add to this problem given the window for any new tasks to safe tax credit is so small,” Connelly stated. “The passage of laws in new markets might doubtlessly add upwards of 1.1 GWDC by means of 2030.”

New state markets might convey extra capability to the market, however there was restricted success in passing neighborhood photo voltaic program laws thus far this yr.

“Buyer demand for neighborhood photo voltaic has by no means been stronger, and we’re seeing states step up with historic expansions like New Jersey’s 3,000 MW and Massachusetts’ 900 MW,” stated Jeff Cramer, president and CEO of CCSA. “These vivid spots present what’s potential when policymakers work to unlock capability. On the similar time, this report makes clear the challenges forward — from federal uncertainty to interconnection delays and program caps — that have to be addressed to understand the complete potential of neighborhood photo voltaic and ship the resilient, reasonably priced energy communities are asking for.”

Subscriber acquisition prices declined in H1 2025, however LMI market challenges persist

Credit score: Ampion

Subscriber acquisition prices decreased 5% from the second half of 2024 on common throughout all buyer segments. Company demand for neighborhood photo voltaic stays excessive, driving up business photo voltaic’s share of complete neighborhood photo voltaic capability to 53%. Nonetheless, builders and subscription administration corporations face elevated headwinds in subscribing low-to-moderate earnings (LMI) prospects. Troublesome subscriber acquisition dynamics lowered the share of neighborhood photo voltaic capability serving LMI subscribers to 9%. The client phase stays the most expensive to subscribe at $102/kW in comparison with $72/kW for non-LMI residential prospects.

As new neighborhood photo voltaic packages wrestle to take off, neighborhood photo voltaic builders more and more goal different distributed photo voltaic packages as pathways for long-term development.

“Non-residential distributed photo voltaic, which usually encompasses tasks sized between 2 to twenty MWDC, is extraordinarily well-positioned for development,” Connelly stated. “Utilities are more and more appreciating the worth of community-scale sources as a result of they are often deployed shortly, with storage and near buyer load.”

Cumulative neighborhood photo voltaic installations at the moment complete 9.1 GWDC and are projected to exceed 16 GWDC by 2030. Wooden Mackenzie has developed high- and low-case situations to explain market uncertainties:

- Excessive case: An 18% uplift to the five-year outlook by means of favorable state coverage modifications and environment friendly interconnection reform, including 1.3 GWDC

- Low case: A 16% contraction resulting from complicated tax credit score qualification tips and restricted state intervention, decreasing outlook by 1.2 GWDC

Information merchandise from Wooden Mackenzie