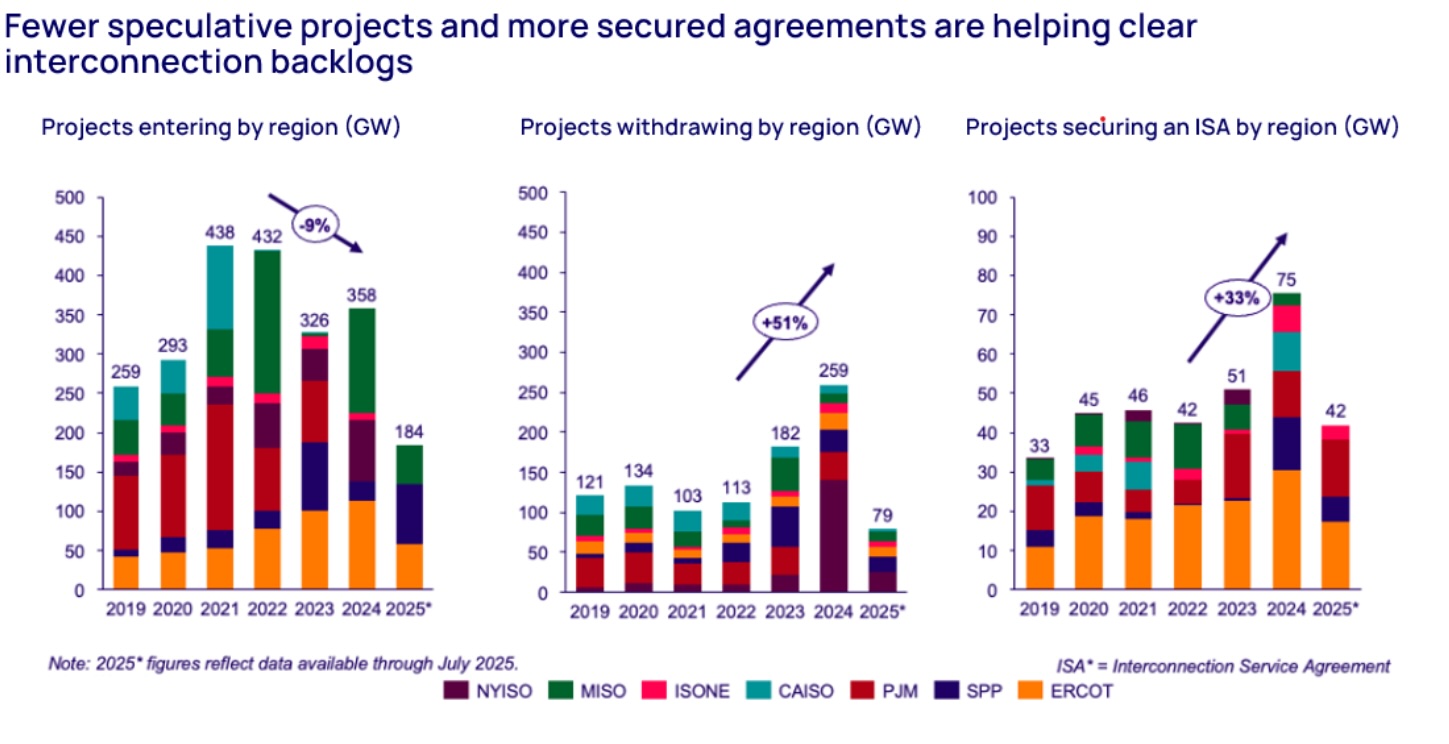

United States grid interconnection agreements reached historic highs in 2024, surging 33% to 75 GW — the best quantity on file — resulting from new federal laws aimed toward streamlining the method, in response to a brand new report from Wooden Mackenzie.

In response to the report “Tracking the progress of US grid interconnection,” information from Wooden Mackenzie’s Lens Energy and Renewables platform exhibits that Federal Vitality Regulatory Fee (FERC) Order No. 2023, issued in July of 2023, together with different reforms led by Unbiased System Operators (ISOs), has made a substantial influence on processing interconnection agreements, by driving enhancements via lowering speculative initiatives and clearing queue backlogs.

On high of elevated connections, regional grid operators are experiencing 9% fewer new undertaking entries, a 51% improve in withdrawals of non-viable initiatives since 2022.

“It’s clear that these reforms are displaying early indicators of promise in accelerating the tempo of interconnection research,” mentioned Kaitlin Fung, analysis analyst, North America Utility-Scale Photo voltaic for Wooden Mackenzie. “We noticed a file 12 months in 2024, with 75 GW of secured capability. 2025 is sustaining this momentum, as main grid operators have already secured 36 GW via July 2025, positioning the 12 months to match 2024’s file.”

Photo voltaic and storage proceed to dominate secured interconnection agreements

Photo voltaic and storage applied sciences captured 75%, or 58 GW, of all interconnection agreements in 2024 and can retain the same market share in 2025. Photo voltaic has accounted for half of all signed IAs since 2019, a pattern that continues in 2025.

Pure fuel has seen a rise in interconnection requests since 2022, including 121 GW of capability. This pattern has continued in 2025 with new functions for fuel era already breaking annual data by mid-year. Nonetheless, the variety of profitable fuel interconnection agreements is down 25% since 2022, primarily in PJM, MISO and ERCOT.

Regional variations

“Interconnection success charges and queue processing occasions fluctuate dramatically for various grid operators throughout areas,” mentioned Fung.

In response to the report, ERCOT leads in each success charges and processing pace resulting from its streamlined queue course of via their connect-and-manage method. ISONE ranks second in success charges however has the longest processing time resulting from its delayed transition from serial to cluster-based processing. CAISO ranks third, however has one of many lowest success charges, pushed by a excessive quantity of speculative initiatives.

“Whereas we’re seeing constructive momentum, important challenges stay,” added Fung. “Pure fuel initiatives are coming into queues at file ranges however declined in annual signed interconnection agreements since 2022, and regional disparities in processing occasions spotlight the necessity for continued reform efforts.”

Information merchandise from Wooden Mackenzie